World Bank's Nigeria Development Update... Ongoing Reform Drives: A Mixed Blessing?

An Extraction of the Afrinvest Weekly Economic & Market Report for July 7, 2023

Photo Credit: The Cable

This week, our focus is on the June 2023 edition of World Bank’s National Development Update (NDU), titled “Seizing the Opportunity”. In this report, the World Bank (WB) lauded the current administration’s removal of the fuel subsidy and foreign exchange (FX) management reforms, describing the policies as crucial measures to rebuilding fiscal structure and restoring macroeconomic stability. The World Bank expects the reforms to brighten the 2023 growth outlook (estimate of 3.3%) compared to the prior year (3.1%). Nonetheless, growth performance would trail those of other oil-producing peers.

Similarly, the transition towards a more unified and market-responsive exchange rate is expected to boost FX supply in the market, enhance the confidence of FPIs & domestic investors, and improve trade & capital flows. Also, the removal of the fuel subsidy is expected to increase price pressure in the near term but significantly rein-in inflation in the medium term as well as improve FG’s fiscal capacity. For context, the government is projected to achieve fiscal savings of about ₦2.0tn in 2023 – accounting for 0.9% of GDP. These savings are expected to reach over ₦11.0tn by the end of 2025 if the reform is not reneged on.

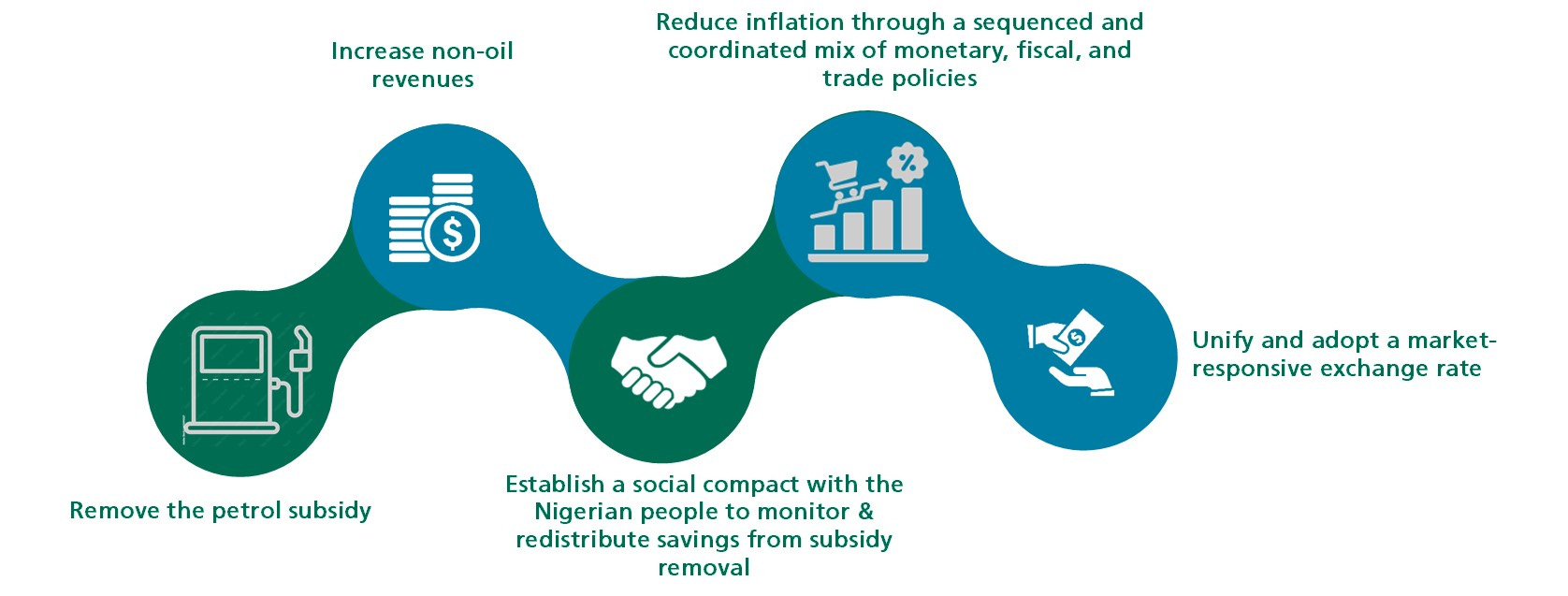

Chart 1: Snapshot of World Bank's Recommended Reforms

Source: World Bank, Afrinvest Research

Despite the numerous potential gains that should emanate from the ongoing fiscal and monetary policy reforms in a no-distance period, the Bretton-Woods institution highlighted that the reforms must be accompanied by compensatory measures to alleviate the short-term impact on the poor and the most vulnerable. Specifically, if proper soft-landing measures are not put in place, the WB estimates that additional 4 million Nigerians (one of the highest among oil-producing peers) could slide below the poverty line by the end of 2023. By implication, this increase would bring the total number of Nigerians below the poverty line to 136.9m, given current estimates of 132.9m as of 2022 year-end.

The devaluation of the official exchange rate is anticipated to have significant implications for Nigeria’s Public and Publicly Guaranteed (PPG) debt stock. According to WB, Nigeria’s PPG debt-to-GDP ratio is expected to touch 46.0% in 2023, previously 40.0% in 2022. In order to maximise their shared impact on growth, job creation, and poverty reduction, WB recommended some critical measures in two key areas which align with our prognosis for an effective reform as captured in our 2022 Banking Sector Report. First, in order to restore macroeconomic stability, Nigeria needs to attend to the vulnerability of the economy to shocks (domestic and foreign) – a prerequisite to accelerating growth, reducing poverty, and boosting job creation. This can be achieved by increasing non-oil revenue and reducing inflation through a sequenced and well-coordinated mix of monetary, fiscal, and trade policies.

Second, the WB recommended the establishment of a redistribution mechanism that uses a portion of the fiscal savings to protect lower-income households and minimise the negative impact of the subsidy removal while still supporting the government’s revenue target. In our opinion, WB’s call for timely introduction of safety net is instructive, given that growing number of people below poverty line can derail economy growth from its full potential due to weak aggregate consumption and low per capita income. In addition to the WB’s recommendations, we posit that the current administration should put in place mechanisms to curb oil theft, reduce the cost of governance, and improve its current tax reforms to achieve the desired outcome.

Global Equities Market: Advanced Market Rout Dampens performance

In the US, Institute for Supply Management Purchasing Managers Index (ISM-PMI) showed that manufacturing sentiment weakened for the eighth straight month in June as a mix of tight credit and weakening purchasing power hit the sector. The index dropped to 46 index points – indicative of contraction – against 46.9 index points recorded in May. A disaggregation of key PMI components showed that Production and Employment indices fell to 46.7 and 48.1 against 51.1 and 51.4 respectively. Also, the decrease in Price index from 44.2 to 41.8 suggested sellers were willing to lower prices to a ensure steady stream of new orders. Elsewhere, minutes of Fed's June FOMC meeting suggested that the interest-setting committee might vote in favour of a hike in July, resuming its tightening campaign despite positive inflation trajectory. The combination of weak economic outlook, possible rate hike, and still-tight job market (+209,000 new non-farm payroll jobs in June) weighed on market sentiment, pulling the S&P 500 and NASDAQ indices 0.8% and 0.5% lower w/w respectively.

In the UK, the S&P Global/CIPS Services PMI fell to 53.7 in June against the previous reading of 55.2 – an indication that business confidence is diminishing, although the overall outlook remains positive. Inflation concerns remained on the front burner as UK stood out as the only G7 country where consumer prices have maintained an uptrend. Similar to the US and UK, Composite PMI Output Index (by Hamburg Commercial Bank) fell to a 6-month-low of 49.9 in June (May: 52.8), with Services PMI Business Activity Index down by 3.1 points to 52.0. Consequently, UK’s FTSE, France's CAC 40, and Germany's XETRA DAX indices declined by 3.4%, 3.8%, and 3.4% w/w respectively. In the BRICS markets, performance was bearish, except for India’s BSE Sens and Brazil’s Ibovespa indices which gained 0.9% and 0.5% each.

The performance of the African, Asian, and Middle Eastern markets were largely positive supported by country-specific factors, capital flow reversal to Emerging Markets (EMs), and resilient commodities market performance. In the coming week, we expect sentiment to wane as risk-off posture intensifies due to expected Fed hike.

Domestic Equities Market: Bulls Sustain Momentum … ASI up 3.4% w/w

Buy interest dominated across all sectors this week on the local bourse, as optimism continued to drive bullish momentum. Consequently, the NGX-ASI rallied 3.4% w/w, market capitalisation improved ₦932.2bn to ₦34.3tn, while YTD return advanced to 23.0% (previously: 19.0%). Activity level strengthened as average volume and value traded rose 155.0% and 110.0% w/w to 2.0bn units and ₦29.1bn respectively. Top traded stocks by volume were FCMB (566.3m units), FBNH (516.3m units), and ACCESSCORP (356.2m units), while FBNH (₦90.0bn), ACCESSCORP (₦6.3bn), and UBA (₦4.6bn) led in terms of value.

Assessing the sectors under our coverage, performance was bullish as 5 indices gained while the Consumer Goods index lost 0.2% w/w due to price erosion in NESTLE (-4.0%) and FLOURMILL (-0.9%). The Banking index led the gainers with a 9.8% w/w increase, owing to a price surge in UBA (+15.9%), FIDELITY (+27.6%), and FCMB (+30.4%). The Oil & Gas and Industrial Goods indices rose by 7.2% and 2.2% w/w respectively, following buying interest in ETERNA (+35.2%), CONOIL (+23.3%), and DANGCEM (+5.3%). Similarly, the Insurance and AFR-ICT indices gained 0.7% and 0.5% w/w accordingly, driven by price uptick in CHIPLC (+57.3%), LINKASSURE (+7.1%), and MTNN (+0.6%).

Investor sentiment, as measured by market breadth, improved to 1.1x (previously: 1.0x) as 79 stocks gained, 23 lost and 57 remained unchanged. Notable gainers for the week were JAPAULGO (+58.6%), CHIPLC (+57.3%), and CHAMS (+56.8%), while WAPIC (-26.5%), TRIPPLEG (-26.4%), and LASACO (-16.9%) led the top losers. In the coming week, we anticipate the bullish momentum to continue due to positive sentiment.

Foreign Exchange Market: Stronger Naira Across Windows

At the end of the trading week, the average Brent crude oil price rose 2.9% w/w to $76.35/bbl. This could be attributed to an increase in demand levels for the third consecutive time as reported by the EIA in the US. Also, supply concerns following production cuts from Russia and Saudi Arabia helped overturn the recent bearish sentiment. Meanwhile, Nigeria’s foreign reserves fell 0.4% w/w to $34.1bn as of July 5th, 2023.

At the parallel market, the base currency (dollar) depreciated 3.1% w/w against the price currency (Naira) to ₦748.00/$1.00. While at the Investors’ & Exporters’ (I&E) Window, the base currency (dollar) fell 0.9% w/w against the price currency (Naira) to ₦762.63/$1.00 as the market continue to price in the recent FX policies. Meanwhile, activity level rose by 10.8% w/w to $630.7m at the end of the week.

At the FMDQ Securities Exchange (SE) FX Futures Contract Market, the total value of open contracts remained unchanged at $6.8bn due to the CBN rendering contract tenors within a year inactive due to ongoing FX reforms. In the coming week, we expect rates across different FX segments of the market to trade within a tight band.

Money Market: Secondary T-Bills Market Trades Bullish

At the beginning of the week, OPR and OVN rates opened at 1.1% and 1.6% respectively, lower than last week’s close of 1.4% and 2.0% despite a decline in system liquidity owing to the settlement of the PMA held on 30th June. During the week, maturities worth ₦5.0bn boosted system liquidity. As a result, OPR and OVN rates fell to 0.9% and 1.3% w/w respectively as system liquidity settled at ₦720.1bn.

In the secondary market, performance was bullish as rates across maturities declined 83bps w/w to 5.3% following strong demand as system liquidity remained buoyant. Yield on the 182 and 364-day instruments fell 169bps and 104bps w/w respectively while yield on the 91-day instrument rose 25bps w/w to 5.2%. Although we do not expect any inflows in the coming week, system liquidity is expected to remain high. We also expect sustained demand interest in T-bills to persist.

Bond Market: Mild Gains in the Local Bond Market

The domestic bond market closed the week on a mildly positive note following gains on two of the five trading days. Consequently, average yield fell 2bps to 12.6% backed by buying interest in the long tenors as average yield dipped 25bps w/w. Meanwhile, average yield on short and mid-end bonds rose 41bps and 10bps w/w respectively.

The risk-off sentiment in the SSA Eurobonds market resurfaced this week following a downbeat performance as average yield climbed 211bps w/w to 62.2%. This return was largely due to a surge in yield on bond close to maturity - Nigerian 2024 instrument (yield up 338bps w/w). Also, the Zambian 2024 bond saw sell pressure as yield rose 802bps w/w.

In a similar stride, performance in the Corporate Eurobonds space under our coverage waned this week as average yield increased 4bps to 15.6%. Yield uptick on the EBN FINANCE and ECOBANK 2024 instruments, up 43bps and 22bps respectively majorly drove the weak performance.

In the coming week, we expect the domestic bond market to be guided by liquidity play. For the Eurobonds market, we do not foresee a major catalyst offsetting investors’ weak sentiment, hence we expect a bearish performance.