Afrinvest Weekly Update | Cardoso’s Sectoral Speech… Economic Silver Lining or Vague Optimism?

An Extraction of the Afrinvest Weekly Economic & Market Report for February 9th, 2024

Photo Credit: CBN

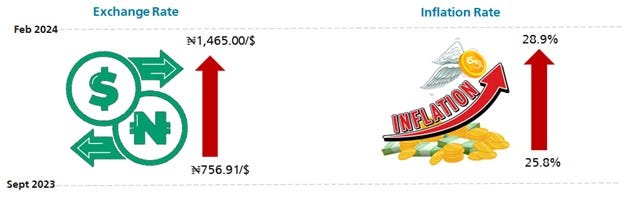

This week, we focus on the CBN Governor, Mr. Cardoso's speech during his appearance at the sectoral debate of the National Assembly on Tuesday. The CBN governor was summoned by the House of Representatives on the back of declining economic fortune highlighted by the continued free-fall of the Naira and unabating price pressure. Recall that the Naira official rate tumbled 37.7% in January against the greenback to exchange at ₦1,455.59/$ (the pair had earlier lost 49.2% in 2023 to rank among the top five worst-performed currencies globally) while the headline inflation rate reached a 3-decade high of 28.9% in December 2023 with little hope of a respite in the near-term.

In his speech, Mr. Cardoso re-emphasized his previous claims that Nigeria has reached an inflection point and that the ongoing critical reforms across various segments would tackle longstanding legacy issues. He highlighted recent upgrades in credit ratings by international agencies (Fitch and S&P) and commendations from Bretton-Woods institutions as proof of reform progress. Regarding the domestic economy, the apex bank governor aligned with FG's 3.8% growth projection for 2024, a 110bps outrun to the 2023 estimated performance. This optimistic outlook is based on expected gains from increased crude oil production, higher crude prices, and ongoing reforms. Furthermore, on inflation, Mr. Cardoso expects the average headline rate to ease to 21.4% in 2024 from 24.5% in 2023. Lastly, on the exchange rate, the CBN governor blamed Naira pressure on the simultaneous increase in USD demand for education, healthcare, and imports alongside declining supply.

As per the way forward, the CBN Governor noted several strategies are in place to enhance liquidity and price discovery in the FX market. These include unifying FX market segments, clearing outstanding FX obligations, introducing new BDC operational mechanisms, and enforcing banks' Net Open Position (NOP) limit amongst others. Recall that Mr. Cardoso in an interview earlier in the week stated that out of the $7.0bn FX backlog inherited, the CBN had cleared $2.5bn in verifiable claims, with $2.2bn outstanding and $2.4bn having irregularities. The Governor noted that all these measures would stabilize the exchange rate, deepen the FX market into a more market-oriented mechanism, and restore investors' confidence in the financial markets.

In our view, the CBN governor’s bold stance that Nigeria may have reached an economic turning point given ongoing reforms is premature. We note that the sort of fiscal and monetary policy cohesion and shared vision that should deliver a turning point is yet to be birthed. On the back of this, we hold that the 3.8% growth projection for 2024 by Mr. Cardoso may prove elusive (Afrinvest projection: 3.0%) given the lack of noticeable improvement on key pain points in the business environment, incessant insecurity in the agrarian communities, and underwhelming crude production as well as the lingering “wait and see” approach of foreign investors towards Nigeria. As per Mr. Cardoso’s expectation that the average inflation rate would ease to 21.4%, we think that growing downside factors – disruption of food production and supply by insecurity, poor infrastructure, and Naira free-fall – could derail the expectation even though high base effect has provided sufficient legroom for the headline rate to moderate on a year-on-year basis.

Finally, on the exchange rate, we flag that the CBN governor might be looking at the wrong side of the spectrum in emphasising dollar demand for services and imports as the root causes of the declining Naira, given that demand for services and imports would always exist if not readily available in the country. Moreso, a chunk of these travellers eventually morph into diaspora workers who remit FX back into the country (remittance remains the most resilient source of FX inflows to date). Therefore, blaming the current FX crisis on demand-pull factors might be a distraction in tackling the issues affecting supply. We opine that the CBN should instead focus on reforms that would restore confidence in the market and boost major FX inflow channels. In light of this, we applaud the CBN’s continued work to clear verifiable FX backlogs as it is a much-needed step in the right direction to restore confidence in the market. Also, the narrowing of the negative real rate of return as evidenced by the upward repricing of yields at the recent NT-Bills auction is commendable. However, we reiterate that closer coordination with the fiscal leg is needed to curb excess liquidity given that money supply (M3) grew 51.0% y/y to ₦78.7tn at the end of 2023. Overall, we maintain that Nigeria’s 2024 economic performance will be hinged on the extent to which the fiscal and monetary authorities follow through on reforms harmoniously.

Chart 1: Exchange & Inflation Rate Dynamics Pre & Post Cardoso Administration